Over the last few months we have encountered heightened volatility in the bond market. Although Treasury yields had been increasing in front of a mid-June speech by Fed Chairman Bernanke, they have continued to run to the upside post the commentary without a whole lot of retracement up to this point. Heated Fed backpedaling since mid-June has succeeded in lifting equities to new heights, but not so bonds. I’d like to discuss two topics I believe important. First, just what is the bond market discounting right now?

Secondly, equity bulls have again resurrected the “great rotation” story as of late. You’ll remember comments about this that made the rounds early this year, the thesis being investors were on the cusp of “rotating” from bond holdings to stocks. So far this year, the mutual fund flow numbers have not validated this theory. Will they ahead as bond prices have now run into a bit of turbulence? To answer this question, I’ll look at large institutional capital allocations of the moment. Just which investor groups have large bond holdings that could theoretically be sold as a potential funding source for stock purchases and what is the likelihood this “rotation” will occur?

With any type of investment, it’s always important to think about just what the financial markets are discounting in price at any point in time. In terms of bonds, perhaps the information “new” to the market over the last month is that the Fed’s Quantitative Easing (QE) program is not going to last forever. To be honest, we knew this all along; we just had not heard Bernanke say it out loud. Well now we have. So in good measure the US fixed income market is attempting to discount in current bond prices just what will transpire with the Fed’s QE policy over time. Will they slow down their $85 billion per month bond purchases in September of this year or will that occur in 2014? Will they “taper” (the latest buzzword) purchases over time, and if so in what magnitude? Certainly these questions remain to be answered. The volatility we are seeing in bond prices is a result of lack of clarity and specifics. Although this is nothing new, bond investors are now attempting to discount a future that has become more uncertain post Bernanke’s comments last month.

Personally, I’m wary of yet another issue related to the above that may also be getting into bond prices right now. I’m very wary that the markets may be starting to question Fed credibility, the expression of which is downside volatility in bond prices. Think about it. Over the last few months, we have been treated to so many conflicting policy comments coming from Fed members that I’ve lost count. I’ve been personally convinced that a Fed who cannot lift interest rates right now (as Bernanke told us in recent testimony, “the economy would tank” if the Fed raised rates) will use “jawboning” to attempt to influence financial market behavior. We saw many a Fed member talk about QE curtailment over the mid-May through June period. Were these Fed members trying to cool down perhaps too hot equity and commodity markets with tougher talk? If they were, it had no effect as it took Bernanke mentioning possible QE curtailment for investors to listen and both equity and commodity prices to temporarily correct. But in the wake of this correction, Fed members immediately backpedaled on Bernanke’s QE tapering comments as they clearly did not like the very short term market reaction.

Unfortunately, the conflicting comments regarding policy continue to this day. There is no uniform message among Fed members. One day a member suggests QE needs to stop by the end of the year. The next day another Fed member tells us the Fed will remain very accommodative well into next year and beyond. So just which one is it? And how can investors make decisions when the Fed members themselves are delivering conflicting messages intraweek? Is the failure of bonds to rally meaningfully, as have stocks, an expression of initial investor questioning of Fed credibility?

The commentary flip flopping suggests the Fed really has no well-defined plan, let alone magic bullets. They are now simply reacting to short term market movements they have helped create with the all over the map policy quotes in the press. I’ve long wondered that after four years of unprecedented monetary policy with still very tepid at best economic growth, just whether investors would lose faith in the Fed (and really global central bankers for that matter) and politicians. That time may have come. And just how would financial markets price in a loss of faith? We’ll first see it in bond prices. Is this what the failure of bonds to meaningfully rally in the face of recent Fed commentary back pedaling is really all about?

We know that since early 2009, faith in the Fed’s Quantitative Easing policy has been a major support to equity and bond prices. We need to watch bonds closely ahead for a potential expression of a loss of faith that would be seen in price. We may be seeing the initial signs of this right now. If so, what does this ultimately mean for stock prices? We simply need to remember that in many past financial market cycles, credit (bonds) has led equities in terms of price trends. As always, some of the most important market information can be found in price divergences between asset classes such as stocks and bonds. We’re seeing such a divergence right now.

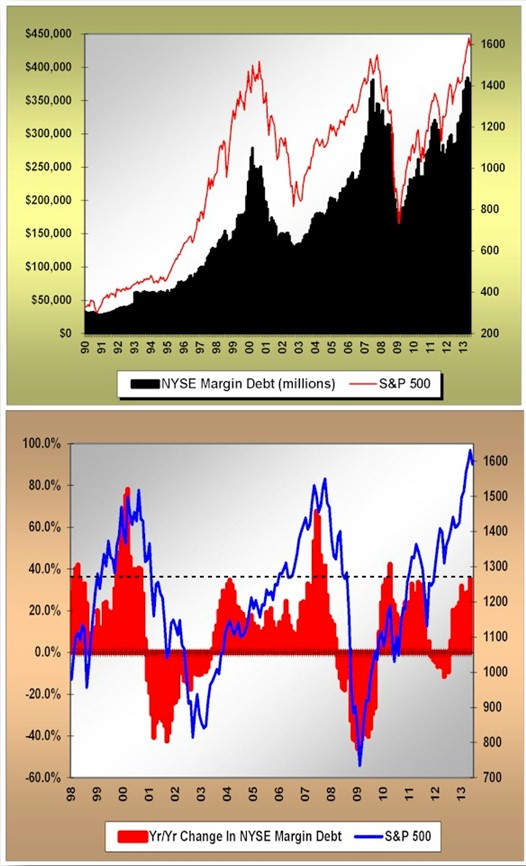

As mentioned, I want to switch gears a bit and come back to the great rotation theme. Will investors heavily exposed to bonds sell and rotate that investment into stocks now that bonds are acting a bit shaky? It just so happens that we also may be getting the beginning of an answer to that question now. We know that over the past four years, many a retail investor has shunned stock investment in deference to purchasing bonds. Not surprising in that retail investors in equities have experienced two major stock market declines within the prior decade. What also is not too surprising is that with the initial volatility we’ve seen in bond prices since May, retail investors have hit the sell button with little hesitation. From mid-May through June month end, retail bond fund investors pulled just shy of $70 billion out of bond funds – a record outflow.

So if indeed we are to see a great rotation from bond investments to stocks, the important question is “just where did this money go?” Over this same period, less than $500 million came into stock funds – that’s right, less than 1% of the money that left bond funds. For now, by far the largest repository we’ve seen for cash created by bond fund redemptions has been money market funds and bank deposits. Together, growth in money funds and bank deposits combined over this period account for all of the proceeds from mutual bond fund sales. That does not mean these assets will not ultimately gravitate to equities, but there is no sign that this has yet happened. For now, the great rotation is an intriguing story that just happens to be lacking factual validation.

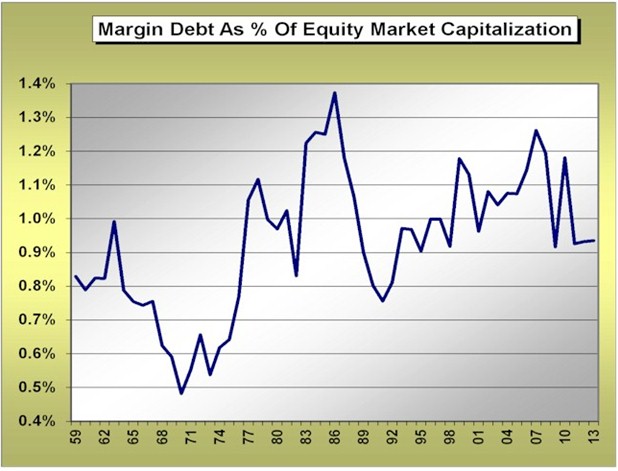

Before concluding, let’s look at the current and historical asset allocation of a number of large pools of investment capital. Are there groups with still heavy exposure to bonds and how likely would it be that this exposure shifts to stocks?

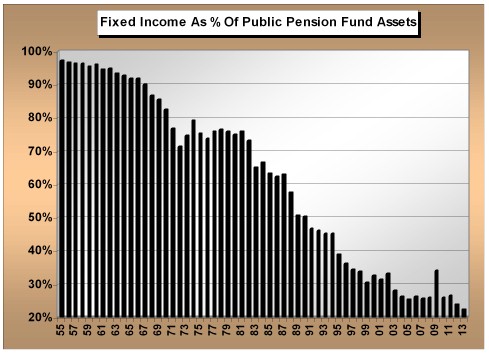

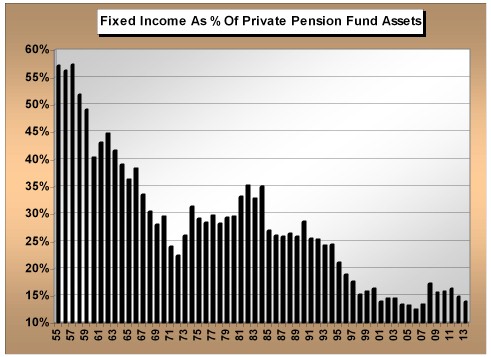

Two larger pools of institutional capital belong to pension funds and insurance companies in the US. The following two charts show us the history of public and private pension fund allocation to bonds.

What the data above show us is that US public (think municipal and government) and private (think corporate) pension funds have the lowest, or close to the lowest, allocations to bonds in over a half century. Haven’t these meaningful pools of capital already rotated away from bonds from an historical standpoint? It sure looks that way. I’ll save you the historical retrospective of insurance companies as their historical bond investment allocation character is almost identical to what you see above.

Banks in the US have always been large holders of bonds, but at the moment bank holdings pale in comparison to the magnitude of bond exposure in the mutual fund complex and bonds held at the household level. Any change in bank investment posture simply cannot move the needle. Moreover, there is little likelihood bank investment in bonds would migrate to equities.

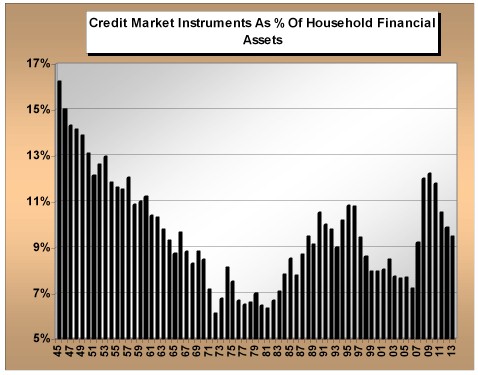

As of the end of the first quarter or this year, outside of the foreign community, US households were the largest owners of individual corporate bonds. Households are the largest owners of municipal bonds. And households are the third largest owner of individual Treasury debt, behind the foreign sector and the Fed itself. So, as we look at household ownership of individual bonds as a percentage of total financial assets, we see the following.

Relative to history we’re in middle ground right here. Yes, households increased their bond ownership in the post 2007-2008 world. But allocation relative to total financial assets remains modest. A tsunami of money to come from household bond holdings just waiting to be liquidated? Let’s just call it a potentially large swell.

That leaves us with the foreign pools of capital. As I’ve suggested in discussions this year, the weight and movement of global capital is one of the most important investment themes of the year. A theme I expect will continue into 2014. It’s no mystery at all that foreign purchases of US bonds have been meaningful support to the broad US fixed income markets for really decades now. In good part this has been a game of mercantilist economics. Trade surpluses generated by foreign countries exporting goods to the US have been “recycled” by these foreign countries into purchases of US bonds. These purchases have helped keep US interest rates low and helped perpetuate US imports of foreign consumer goods. China and Japan have been the poster children for this type of activity.

As of the end of the first quarter of this year, the foreign community is the largest holder of US Treasuries and corporate bonds. Moreover, foreign holdings of all types of US bond investments as a percentage of total foreign holdings of US assets rest just under 50%. Although this is a number near historical highs, by no means is this something new.

If there is any sector that would be a viable candidate for a rotation from US bonds to stocks based solely on the character of current investment allocation, it’s the foreign community. Although it’s a possibility, is it a probability? Most foreign holdings of US bonds are held by “official institutions” – Governments and central banks. As such, their purpose is only partially related to rate of return on investment. Other agenda’s such as cross currency rate manipulation, supporting domestic export industries, etc. are high on the list of priorities for foreign holders of US bonds. A wholesale movement into US equities is not a strong probability, not even close.

The downside volatility we’ve recently experienced in the US bond market is something new for the current cycle. The recent divergence between US bond and stock prices demands attention as we move ahead. This is punctuated by the fact that the Fed is not buying stocks, they are buying bonds, yet stocks have zoomed to new highs while bonds struggle. Are US bond investors beginning to lose faith that Fed monetary policy can right the still listing domestic economic ship? Further rising bond yields would suggest this may be the case. We’re not there yet, but need to be mindful of a potential shift in investor perceptions. In past cycles credit has led equities. Will it be so again?

One other character point of the current year is that investment diversification has hurt. Gold and commodities have struggled. Bonds globally have hit a pocket of price turbulence. Emerging market equities in many cases are gasping for breath. The global investment leaders have been equities in countries whose central banks have engaged in high powered monetary policy – specifically the US and Japan. In the race for investment performance, it’s now a very narrow playing field. Will investors with bond allocations rotate to equities ahead? Institutional asset allocation profiles tell us that many large pools of capital are already sitting with historically low bond allocations. If there is an asset allocation rotation of meaning to come at all, it would be from the foreign sector and to a much lesser degree from US households. So far, neither has shown signs of an asset allocation shift.

Will US bonds “behave” as we move forward? US credit markets are now a key watch point. We know the Fed can control short term interest rates, but even their balance sheet is not large enough to control longer maturity interest rates for any extended period of time. Up until the present, that has been accomplished by “faith in the Fed” – something that may now be on the cusp of important change. How longer term interest rates behave, or otherwise, ahead will be very meaningful to the totality of global investment outcomes.