Investors are painfully aware of Fed Chairman Bernanke’s comments in mid-June on timing the end of Quantitative Easing (QE III). Can it really be that, after imposing a flattened rate environment where obtaining even modest yield is only achievable by seriously increasing investment risk, Bernanke and Co. would literally yank the rug right out from under investors? Investors who have been playing the game by the Chairman’s rules?

The quick answer to that question came by double digit drops in yield oriented asset classes such as utilities and MLP’s, as well as record weekly bond fund outflows. Those merry pranksters at the Fed, they’re always good for a belly laugh, right? What will they think of next?

The Chairman told us that the Fed’s assessment of the US economic landscape has improved. The Fed now expects a 2.6% GDP number for 2013. That’s well ahead of current consensus. As you’ll remember, stated Fed objectives with QE III are improvement in the labor market, a drop in the headline unemployment rate, and a “better” tone to the US economy (without benchmark or quantification in terms of what specifically a “better tone” means). Back in September 2012 when QE III was initiated, the Fed said that they would assess the underlying character of the US labor market in addition to wanting to achieve a headline unemployment rate number of 6.5%. Mr. Bernanke tells us the Fed believes the US labor market has improved.

So, in the spirit of cooperation, I thought we’d do a bit of the Fed’s work for them – going into labor, if you will.

Is it really true that the US labor market has improved? If so, by what metrics and historical context? By the Fed’s objectives, does current US labor market character justify a tapering of bond purchases by the Fed? Please do not mind the fact that the Fed has never once drawn an academic – or any other – linkage between their buying of US Treasuries and mortgage backed securities (MBS), and actual jobs growth. So, just what does labor market “improvement” look like now that so pleases the Fed?

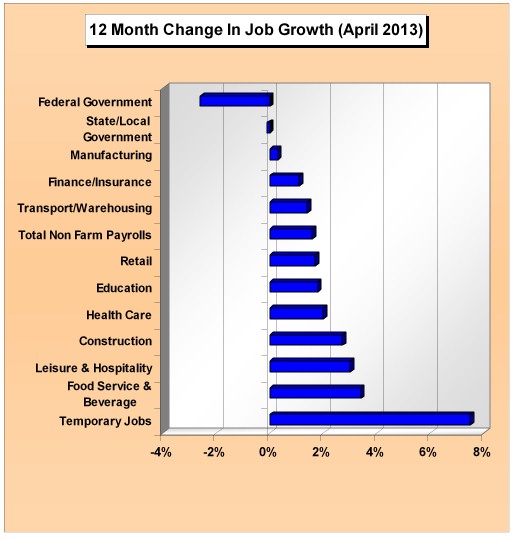

Let’s start with a quick review of where we’ve been over the last 12 months, ten of which fall under the magical QE III umbrella. The following chart chronicles the percentage job growth as per the major labor market employment classifications.

We’re four years into the current economic expansion cycle. Yet in the last year, the largest percentage gains in jobs have been in Temporary positions. Historically, the largest gains in temp positions occur at the beginning of prior economic expansion cycles, not four years into the cycle. That growth in temp jobs stands head and shoulders above more permanent classifications speaks to the continuing tentativeness of employers. Next up in terms of job growth percentage gains are Food Service and Beverage (bars and restaurants) as well as Leisure and Hospitality (hotels). Like Temporary, these job classifications have historically represented lower wage demographic and limited benefits.

Alternatively, where historically we’d look for strong gains in job classifications such as Construction, Manufacturing and Finance/Insurance, those sectors have registered tepid at best percentage growth in the current cycle and over the prior 12 months specifically. (As a quick tangent, year over year gains in total US wages have been bumping along historical lows in the last year.) What you see above helps explain this current cycle phenomenon. This is the labor market recovery that Mr. Bernanke and his FOMC compadres point to with confidence?

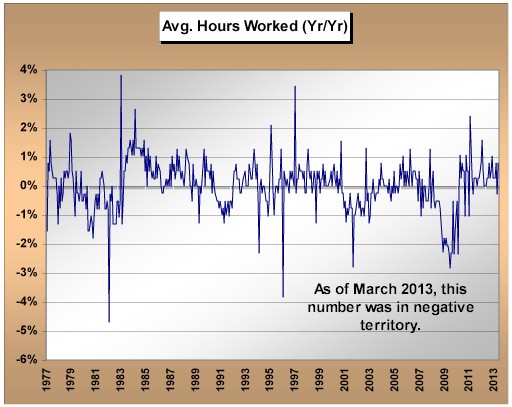

As a bit of a twist over the last 12 months, it is clear that US employers have been anticipating implementation of the many Affordable Care Act (Obamacare) rules and regulations. This has definitely affected the character of today’s US labor market. In March we saw the 12 month rate of change in US average hours worked fall into the deepest negative territory since 2010. Economic expansions are usually characterized by expanding hours worked. The obvious explanation for this is employers’ shift to a greater part time labor force, driven by their desire to blunt the increased cost of health care insurance caused by the Affordable Care Act. While a rational response on the part of employers, this isn’t so wonderful for employees or the economy.

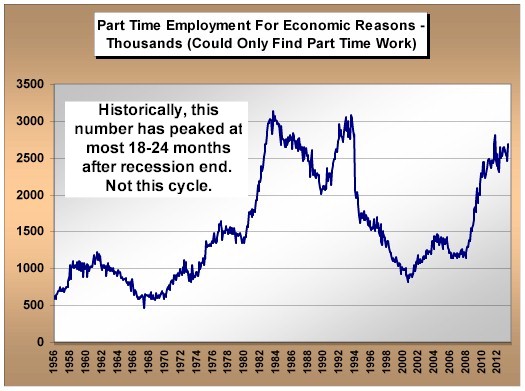

This message by and actual behavior on the part of employers is only reinforced by what you see below. As of April 2013, the number of folks working part time due to the fact that they could not find full time work has risen to almost the highest number in the current cycle (except for a brief spike in 2011).

What is most important in the above graph is that in prior cycles, this employment subset peaked 18-24 months post-recession. But not this time. Except for the brief spike in 2011, we’re still setting new highs four years after the Great Recession officially concluded. Is an increasingly part time US labor force what the Fed envisioned as character point success when they presented QE III as the new remedy for US labor market lethargy?

One last metric deserves your consideration. Over the last four decades, the average weeks of unemployment for the unemployed in each down cycle peaked between 17 and 21 weeks. Naturally this was seen at the worst of each recession experience (and which happened to occur post official recession end in each cycle). As the chart below depicts, we remain at a level roughly double this historical norm – this is new for us. If this does not suggest some structural unemployment in the current cycle, I’m Paul Volcker. No doubt the unprecedented extension of unemployment benefits in the current cycle has encouraged this, since returning to a part time job is less “lucrative” than simply continuing to collect unemployment benefits. Again, this is the character of labor market recovery the Fed has been hoping for in order to scale back QE III?

Is the world coming to an end for the US labor market? Of course not. However, it’s clear that headline nominal job gains do not tell the whole story of the tone of the current US labor market. The Fed knows this. They also know full well that it’s very tough to demonstrate a linkage between their buying of Treasuries and MBS, and actual jobs growth. Is this why we’ve never once seen a Fed member attempt this academic high wire act?

I believe there’s a subplot to Bernanke’s recent comments. Remember, in this cycle the Fed can’t raise rates as in prior cycles to cool down asset classes without derailing a tepid recovery. Thus, the Fed only has its megaphone. Since mid-May, a number of Fed members expressed their somber views on QE III, the need to scale back, etc. That didn’t do much, and minutes prior to Bernanke’s comments, the S&P was less than 2% away from all-time highs with oil closer to $100 per barrel. Markets were not “listening” to them. So was it simply time to bring out the big gun and cool off asset markets running well ahead of either earnings or macroeconomic expansion?

Since it seems all but official that Bernanke won’t be with the Fed come January, does this enable Bernanke to help lay the groundwork for future Fed policy by playing the “bad cop” role? Helping to foreshadow a policy change we all know must come at some point without laying that decision completely at the foot of the next Fed Chair?

We also know that at current rates of purchase, Fed buying has accounted for approximately 80% of all newly issued Treasuries. With the very meaningful acceleration of capital gains and personal income into the fourth quarter of 2012, government tax receipts spiked in the first quarter of this year, and government borrowing has fallen. Unless the Fed tapers a bit later this year, their current rate of Treasury purchases could exceed 100% of newly issued Federal debt. Is this a circumstance the Fed wishes to avoid and can only be accomplished by some measure of tapering, even if temporary?

Lastly, one overriding issue we must not forget is that, despite all the talk concerning QE, labor markets and broader US economy, under QE III the Fed is setting the cost of capital for the Federal government. It’s exactly the same for Japan and Europe right now. Remember, these governments have all borrowed heavily and have not yet begun the process of balance sheet deleveraging. Every 1% increase in interest rates adds about $175 billion to US debt interest costs alone. Will the Fed really turn a blind eye to US interest rates and chance a large increase in Federal interest costs on debt?

As we’ve seen above, it seems very tough to suggest that true improvement in the US labor market is driving the Fed. The Fed is juggling a lot of disparate “agenda” balls in the air with its QE policy – the US labor market is but one. We’ve heard talk in the past from Fed members about an ultimate winding down of QE policy. But I submit to you that the LAST thing central bankers will do is reverse the present course of monetary policy either quickly or abruptly. Why? Because improvement in the US labor market has been lacking, the Federal government has not yet begun a sincere plan of debt reduction, and inflationary pressures remain modest to this day. Change will ultimately come, but very slowly at best. Bernanke and the Fed’s hands are not resting on a light switch, but rather a dimmer switch.