When global central banks began to expand their balance sheets in an attempt to ward off the Great Recession of 2008-2009, their efforts were unprecedented. Never before had we seen so much money creation occur simultaneously on a global basis. At the time, planned central bank quantitative easings (printing money) were well defined in terms of time over which they would occur and magnitude of dollars/foreign currency involved in each QE iteration.

That was then. Despite significant global government borrowing (US Federal debt alone has doubled since 2006) and global central banks printing over $11 trillion since 2008, global economic growth is tepid. In fact, this unprecedented global government borrowing over the last four years has necessitated tax increases in many countries, including the US. The US has sold this as a tax on the wealthy. But when looking at the reality of US Government budget and forward spending projections, there is absolutely no way our federal government can fund its current spending and promises trajectory without very meaningful middle class tax increases to come. Shhh!!! The politicians just have not told anyone yet.

As a bit of a bookend to global central bank balance sheet expansions, we’ve now come 180 degrees from where we were in early 2009. No longer are central bank quantitative easings defined either in terms of time or magnitude – several central banks have recently promised unlimited money printing over an indefinite period of time.

This is exactly what the US Federal Reserve continues to say and do four years into our current economic recovery. The election of Abe in Japan a month ago cements the fact that the Bank of Japan will join in unlimited money printing. The Bank of England is on the cusp of another round of money stimulus. And despite the recent appearance of calm in Europe, banking system recapitalization has not even begun – it will be quite the eye opener in terms of European Central Bank balance sheet expansion to come. Four years after the Great Recession reportedly ended, global central bank actions are pushing the definitional limit of “unprecedented”.

So what has been accomplished by central banks in their historically unprecedented monetary experiment, if not achieving acceleration in economic growth? Well, the nominal level of interest rates rests at generational lows. By pushing interest rates to rock bottom, central banks have raised the net present value of alternative streams of cash flow. In other words, they have been successful at inflating certain asset prices that might not otherwise have risen to their current heights. The US Fed has told us without flinching that they have been directly targeting stock and residential real estate prices. Why? The Federal Reserve believes in what has been termed the “wealth effect”. The thinking goes like this. If asset prices rise, consumers will feel more “wealthy” and will consume at a higher level than would otherwise have been the case. Additionally, consumers might even feel well off enough to borrow and spend if the value of their houses and portfolios rise, exactly as happened during the housing boom of the prior decade. The fact that consumption drives roughly two-thirds of US GDP has certainly not been lost in Fed thinking and actions.

Now that we have embarked on perhaps the final phase of unlimited and indefinite global central bank money printing, will this quantitative easing finally, positively affect the “wealth effect”? Will boundless and limitless promises of money printing do the trick in getting US and global consumers to finally borrow and spend? So far, rising home prices for the last year and rising stock prices for the last four have yet to be the tonic for accelerating domestic consumption. Over the 2007 to early 2009 period, consumer net worth in the US contracted close to $12 trillion. If stock and home prices continue on their current price trajectory, all of this contraction in household net worth will have been recovered sometime this year. Households should be feeling great, correct? So, will it work?

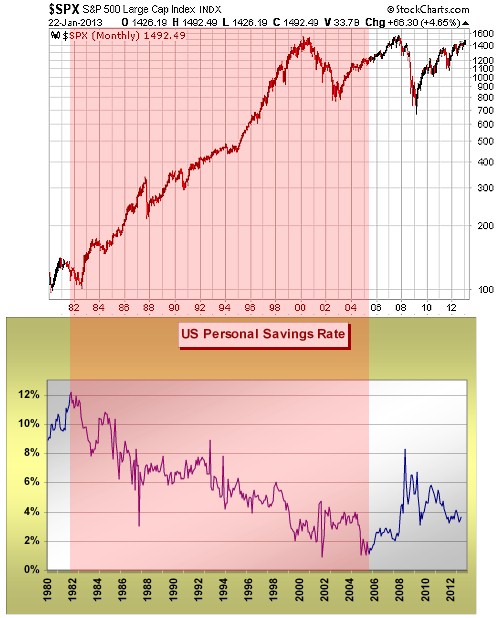

Well, that remains to be seen. Moreover, we question the ability of central bankers to positively affect the so-called household wealth effect (and by implication consumption) by simply printing unlimited amounts of money to levitate residential real estate and equity prices. Why is this the case? Let’s have a look back at some data history I believe is quite important in contemplating this question. For not only does it have bearing on forward potential economic strength, but speaks to where stock and residential real estate prices may head for a time. The graphs below display the US savings rate and the S&P 500 since 1980. The large rise in stock prices from 1980 to present is clear. Intuitively, we also know that over this same period residential real estate prices increased significantly, despite the downturn of the last half decade. Neither of these phenomena should be surprising, as the 1980 to present time frame mimics the coming of age and maturation of the baby boom generation – a generation that bought homes and started retirement plan savings en masse over this period.

What’s important in the relationship comparative graph below is that over the 1980 to roughly 2006 period, the US savings rate declined from 12% to what was a record low near 1%. This occurred while stocks and residential real estate experienced a generational bull market. So let’s step back and think about the concept of a wealth effect – key to current central bank actions. Remember the Fed’s logic reads that if households “feel” wealthier based on rising stock and house prices, they will go out and spend/consume. But this line of reasoning seems to truncate without addressing the key economic question of “spend what?” If stock prices rise, will households sell them and use the proceeds to buy consumer goods? If housing prices advance smartly, will households sell their homes and rent, using the proceeds from the home sale to fund short term consumption? These questions are exactly why the relationship you see below is so important. Over the 1980 – mid-2000’s period, as household “wealth” increased via higher stock and residential real estate prices, it is absolutely clear that households “spent” their savings to consume at a higher level than would have been the case otherwise. We also know households borrowed to consume (remember HELOC loans?)

.

What this historical relationship implies is that for the “wealth effect” to be a positive economic force that spurs consumption, households must have something other than stocks or real estate assets to liquidate and use for consumption, exactly as they did from 1980-2006. They either need to spend their savings or borrow to consume. The key issue of the moment is that at least in the US, savings have not been rebuilt post the Great Recession. As of now, there are no increased savings to spend down while the Fed attempts to make households feel better via their efforts to levitate residential real estate and equity prices. The household savings rate today stands just shy of where it stood in January 2008. I’d again ask the question “spend what?” In the post Great Recession environment, the largest growth in consumer credit has been in student loans, not in revolving or non-revolving credit balances. Households hurt by heavy debt balances, largely related to real estate investments from the prior cycle, have not embarked on a new borrowing cycle. From my vantage point, QE will not positively affect the “wealth effect” and translate into accelerating consumption and domestic GDP growth directly because of the lack of domestic savings, and households remaining gun shy about leverage.

So where does this leave us? It still leaves us with global central bankers committed to unlimited and indefinite money printing, but also a persistent ongoing disconnect between the printing of money and actually getting that money into the real economies globally, as has been the case since 2009. The money they “create” still needs to find a home. And now that we’ve moved into unlimited money printing mode, that means one big home. As a rule, central bankers can create additional liquidity, but they cannot control where or how that money will be put to use. Ideally, they would like to see banks increase lending with this unprecedented liquidity and theoretically get that money into the real economy, but bank lending has been very slow.

Almost as default, that leaves the global financial and commodity markets as a potential repository for historic global central banker largesse. Over the past four years we have heard more than a number of commentators tell us that “the stock market is doing well so the economy must be doing well”. Unfortunately this has not proven to be the case as we continue with one of the most anemic economic recoveries on record. Although we are certainly not there yet, the danger is that this current round of extraordinary excess central banker liquidity creates further asset bubbles, very much as happened with the late 1990’s tech stock bubble and the clear bubble in mortgage lending in the middle of the last decade. By the Fed’s own admission, they missed “seeing” the last two asset bubbles they had a hand in creating. Now that we have moved into the endgame of global central bank monetary expansion, let’s hope central bankers everywhere have had their annual optometrist check-up.