Every once in a while I find it very helpful to just sit back and look at charts that essentially have no titling. At least for myself, it’s often an easy way to “see” trends, or more importantly change in trends, without having my own personal bias of the moment get in the way of trying to interpret what the chart(s) may be telling us. Guess what? Now it’s your turn. Here you go.

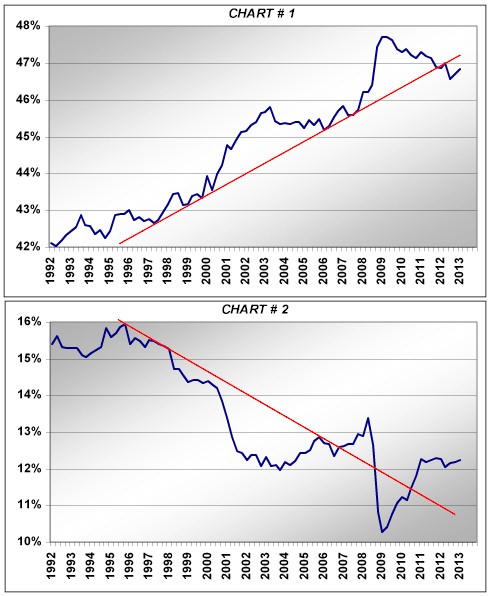

Clearly what we are looking at above are not stock charts as we are not looking at price, but rather percentages, or more precisely percentage contributions as I’ll explain in one minute.

First, as you know, in the middle of last week we were treated to the ISM number for April. Weaker than most would have liked to have seen, but not wildly surprising given recent and obvious weakness in the Chicago and Milwaukee manufacturing numbers. The number came in at 50.7%, not too far from the mainstream vision of the “dividing line” at 50, which theoretically represents the demarcation line between economic expansions versus contraction. A reading below the current has only been seen in 4 months out of the total number of months since the current economic recovery began in the summer of 2009 (two of those came recently in November and December of last year). I will not drag you through an extensive historical retrospective, but the fact is that 50 is not the correct “economic demarcation line” number. If one goes back and looks at all the macroeconomic contractions or recessions in the US historically, ISM numbers in the mid-40’s have characterized such periods. We’ve had plenty of brushes with 50 and numbers just below without a subsequent recession over time. So to suggest that a drop to or slightly under 50 is a major recession warning is incorrect…for now.

Although many have given up on US manufacturing having watched the offshoring of so much former US manufacturing in the prior decade, the fact is that manufacturing has taken on relatively heightened importance in the current cycle for a number of reasons. Okay, Chart #1 you were looking at above is US personal consumption of “services” as a percentage of total US GDP. Remember, we export very few “services” as the bulk of services are “consumed” stateside. Very telling that US consumption of services as a percentage of GDP has been falling consistently over the 2009 to present period.

As you’ve probably guessed by now, Chart #2 is US manufacturing as a percentage of GDP. If these two charts were indeed stock charts, which is the potential buy and which is the potential sell in the current cycle? Without question the US manufacturing sector has been an important sector contributor to overall US economic health in the current cycle and it’s really no surprise as to why. Manufacturing in the US has benefitted nicely from the flood of foreign stimulus unleashed over the last five years by Asia, Europe, South America, etc. Since we do not export services, there has been no such foreign sourced benefit to the service sector.

Additionally, the US service sector has had to weather a domestic household deleveraging environment and very sluggish payroll and wage growth environment. Most probably do not realize this, but the year over year change in the US service sector (as measured by the PCE numbers) in the current cycle is the slowest over the Fed sponsored recorded history of US GDP stretching back into the late 1940’s.

To keep myself honest more than not, the numbers above are the actual nominal numbers as opposed to the real, or inflation adjusted numbers. But even adjusting for inflation, total US service sector recovery in the current cycle has no comparison with prior cycles. Talk about not being able to achieve “escape velocity”, the US service sector in the current cycle is what that characterization is all about.

So in one sense, the relationships you see do not speak to a dramatic US manufacturing recovery, but more of a default environment where manufacturing has done better than services as services are the anomalistic weak standout relative to historical cycles. Just why is this important? Absent meaningful US payroll and wage expansion, it’s a darn good bet the US service sector will continue to remain in tepid water at best. And that puts a big spotlight on US manufacturing looking into the back half of this year and beyond. It should be very common wisdom right now that the US will experience lackluster economic growth in 2Q and 3Q. The initial fallout from sequestration will be felt front and center during those two quarters. But very importantly, consensus thinking on the Street is that the US economy will pick up steam in the back half of the year and into 2014. Important to investment decision making, we see exactly the same pattern with consensus expected corporate earnings right now. Tepid near term growth, but a huge acceleration into the latter part of the year on into 2014. The hockey stick effect is alive and well, as is pretty much always the case anyway. Although I may not be connecting all the dots, it seems reasonable to assume that the non-services portion of the US economy will be very important to the expectation that earnings are about to rocket higher into the back half or 2013 and into 2014.

If the train of logic here is even half right, then it leaves me with a very large, and for now unanswered question. Why are cyclical stocks having such a tough time relative to defensive and consumer oriented equities? Yes, I know all about the “hunt for yield” thesis. Unfortunately, so many defensive and yield oriented equity sectors exhibit valuation metrics of the moment at multi-decade highs that forward investment risk is meaningful. Thanks, Mr. Bernanke, for forcing those who can least afford to accept investment risk (those dependent on investment income) to pay decades high top valuations to achieve very low nominal yields. If you ask me, it’s a very overcrowded trade and one that may end very badly for retail investors myopically focus on stated yields.

The following chart is a look at the Morgan Stanley cyclical stock index versus the Morgan consumer index. We’re resting at what appears quite the important juncture of the moment, now aren’t we? The actual economic numbers tell us manufacturing is important, implicitly suggesting cyclical stocks are a key watch point.

It is absolutely clear that on a relative basis, cyclical stocks peaked in 2011 relative to their consumer brethren, despite the fact that actual US manufacturing as a percentage of GDP has increased since then while services consumption relative to GDP has declined.

Hopefully without trying to force fit relationships, there are two other assets whose charts look a heck of a lot like the one above from 2010 to present. First, without the titles.

With the prices in the charts, you can guess them. Top chart is gold and the bottom copper.

I suggest to you it will be very important to monitor the health of US manufacturing ahead. A good chunk of forward consensus US corporate earnings expectations depend on it. In a forward discussion I’ll come back and look at US port statistics in an effort to further gauge the vibrancy of global trade, and by implication the health of US manufacturing. If the chart above of the Morgan cyclical versus consumer equities breaks the lows it rests upon, I suggest to you it will meaningfully call into question the hockey stick consensus US corporate earnings expectations for latter 2013 and into 2014. Oh well, I guess it’s a darn good thing the Fed has told us they may print even more money ahead. Stay tuned.