In June of this year Fed Chairman Bernanke first publicly discussed the possibility that the Fed would begin “tapering” their Quantitative Easing program somewhere in the near future. Since that time, conflicting commentary from Fed members and hangers on have kept investors guessing as to actual policy outcomes. In addition, Fed commentary alone had caused real global capital to recede from QE beneficiary risk assets such as emerging market equities, bonds and currencies as well as precious metals, commodities and developed economy fixed income vehicles. Although the Fed assured markets their potential QE tapering actions would be incremental, investors have a funny way of discounting tomorrow today.

We know now that when mighty “Casey” Bernanke stepped up to the plate on that fated Wednesday that was September 18, he adjusted his stance, surveyed the playing field and he took a mighty swing…and a miss. No QE tapering on this fine day. Since his original June speech, the capital markets had priced in a September tapering. It had become consensus thinking among investment strategists. The San Francisco Fed had even produced a white paper just weeks before the September Fed decision supporting the view that QE has been largely ineffective in stimulating actual GDP growth. To their credit, the Fed had successfully shaped market perceptions and behavior to expect the beginning of the wind down of what has been an extraordinary, very controversial and historically unprecedented period of US monetary policy. It was the perfect time to deliver the first tapering pitch. Yet at the last minute the Fed decided to throw the markets and investors a monetary curve ball. So much for Fed transparency, clarity and consistent forward guidance for now.

Just what has the Fed really accomplished by postponement? Why might they have taken a pass on tapering their money printing and bond buying now?

I personally believe tapering postponement buys the Fed very little. But from the start, the Fed has told us they were “data dependent” in terms of the tapering decision. In truth, from the standpoint of data alone, postponement actually makes some sense. Payroll employment growth has not exactly been gangbusters as of late and neither has headline GDP growth – both perceptual Fed targets for improvement at the outset of QE3.

Yet we know that the unspoken truth on the Street is certainly that the unemployment number has been skewed in the current cycle by the labor force participation rate, bringing into question the targeting of the unemployment rate in the first place. The chart below is quick look at the history of what is termed the labor force participation rate. What it tells us is the percentage of the population in the total US labor force – those actually working and those looking for work. The clear anomaly for some time now has been the dramatic fall in this number.

Importantly, we need to remember that when folks no longer receive unemployment benefits, they are no longer counted in the official labor force numbers. The labor force count at any time is the denominator in the employment rate relationship that measures those with a job as a percentage of the total labor force. All else being equal, when folks fall off the unemployment benefit rolls, the labor force count falls, the employment rate ratio rises and the unemployment rate falls – none of this having anything to do with actual jobs being created, but rather a lot to do with those losing longer term unemployment benefits.

Just why is the labor force participation rate falling? At least in meaningful part, structural unemployment. We see this directly in the low skilled labor pool. A number of jobs simply disappeared in the last recession for those with low skills. Those working part time due to inability to find a full time job is near new highs for the current cycle. The number of weeks out of work for those who find themselves unemployed is today higher than any recession peak of the last three decades. Point being, it is more than widely known that the unemployment rate itself is a very controversial number in terms of accurately characterizing US labor market slack, yet it is supposedly a headline Fed QE decision making barometer. In one sense, the Fed is shadowboxing an illusion. Question being, how will the continuance of full on QE 3 for a number of additional months change the reality of the current US labor market?

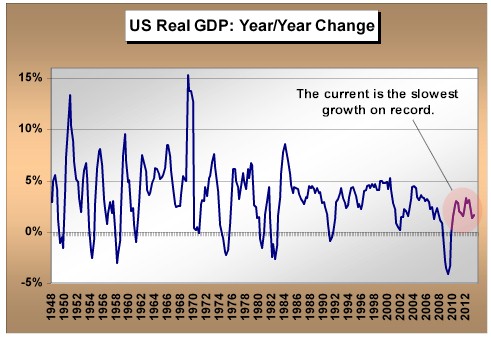

For now, much the same can be said for the macro economy itself. I won’t dwell on this as the numbers are more than well known. The current cycle has consistently shown us the slowest quarterly GDP growth on record for a continuous economic expansion cycle. Not once have we yet been able to achieve 4% annualized real growth in any one quarter – a record over the history of US GDP data

Since the Fed started QE3, growth rates in both payrolls and headline GDP have slowed. Rationale for a postponement of QE tapering? Sure. But again, what will additional QE spark in hoped for acceleration in labor markets and the general economy that the first $3 trillion in QE over the past five years has not already? Exactly what does the Fed accomplish by postponement?

Switching gears a bit, if we believe the ability of QE to meaningfully impact payrolls and GDP over the short term is relatively small, exactly why may the Fed have passed on tapering QE in September?

I personally have two answers hopefully closer to the heart of the moment – interest rates and the debt ceiling political melodrama in which we now find ourselves. It’s a good bet Bernanke and the Fed got a bit more than they bargained for with May rumblings of tapering and the actual mid-June Bernanke tapering dialogue in terms of interest rate movement recently. The ten year US Treasury yield lofted from 1.6% to just over 3% during the May to August period. Importantly, the 10 year Treasury yield is the reference rate against which most 30 year conventional mortgages are based. Conventional 30 year mortgage rates rose to 4.75% in late August from 3.5% or lower in May. This was certainly something the Fed did not want to see as housing has been one of the economic bright spots as of late.

It is interesting to note that the FOMC commentary with the no taper decision began by citing “tightening financial conditions”. At the time, the stock market was near an all-time high, certainly not a “tight” financial condition. In recent quarters we had seen the Fed sponsored Senior Bank Lending Survey show us the easiest of lending conditions for banks over the current cycle to date – certainly not tight. Undoubtedly, the Fed was referring to what had occurred with the general level of interest rates since their tapering commentary began. The taper trial balloon the Fed had allowed to ascend skyward caused a real world reaction in interest rates certainly not to their liking.

Again, what does forestalling QE tapering now mean to forward interest rates? Will bond investors be more accepting of tapering in the future, without sparking such a violent reaction in rates to the upside? The fact is that QE 1,2, Operation Twist, and QE 3 have been in operation over 91% of the time since late 2008. What began as an emergency operation 5 years ago has now morphed into a program of ongoing subsidization. We know the Fed has been the dominant buyer in Treasury and mortgage backed markets for some time. Key question being, will natural bond buyers return to the fixed income markets when a return to free market pricing has been further delayed by Fed inaction? Natural buyers will not return until they can be assured of non-interventionist pricing. We’re still a long way away from such a market environment.

Finally, it’s also a darn good bet the Fed chose to stand down in September due to the debt ceiling political theatrics we have again been treated to in recent weeks. Bernanke directly mentioned that “Federal fiscal policy continues to be an important restraint on growth” in his comments. Tax rates are going higher amidst a slow growth economy. Moreover, components of the Government sequestration process agreed to in early 2013 become effective in early 2014 – there are more Government cutbacks to come that will add up to just shy of 1% of GDP. Of course the irony is that the current debt ceiling debate does not address any of the very important longer term fiscal issues that face the US such as Medicare funding and other booming social costs that lay ahead – these issues are not even on the table.

As investors we simply need to realize that lack of clarity from the Fed may be with us over the remainder of the year and into next. Conflicting Fed commentary has only continued post the no tapering decision. It is generally believed that Bernanke will retire from the Fed in January of next year, but that means that we’ll need to see the President nominate a new chairperson, they will have to be vetted and the Senate will need to approve the nomination all in the next ten weeks (prior to holiday recess). We also have another FOMC policy meeting in December. (I’m assuming the October meeting will produce zero change in policy.) Short term market volatility around these events would be more than understandable.

Yet longer term the question of a wind down and ultimate termination of QE is not going to simply fade away. What began as a needed emergency shot of adrenaline to the heart of the economic patient in late 2008 has now become a continuous IV drip the academicians at the Fed for now deem unacceptable to moderate, let alone remove. QE has been a “subsidy” to both the economy and financial markets. Do Fed policy makers really expect a quiescent market reaction to the potential removal of THE key subsidy of the current economic and financial market cycle? Of course the answer to that question lies somewhere in our now data dependent future.